The latest trends of the tilapia at the beginning of 2026.

The beginning of 2026 should be the time for a new round of fish fry stocking, but so far, the stocking volume has decreased by 20-30%. All fish farmers are betting on a future price rebound. However, prices fell instead of rising at the end of January, reaching a new historical low. The tilapia market situation did not see a price increase despite the reduced supply, which is due to multiple factors: exchange rates, overseas inventory, and the structural dependence of Chinese tilapia exports.

Farmers were hoping that prices would rise as supply decreased, but this was not the case. In the fourth week of January 2026, the price of tilapia raw materials (500-800 gram specifications) supplied to processing plants in Guangdong fell by 0.10 yuan/500g compared to the previous week, setting a new historical low. Although prices in neighboring Hainan and GuangXi provinces remained temporarily stable, they were also at historical lows. This price drop occurred during a period when the number of fry stocked in winter had already decreased, making it particularly "unusual."

Industry analysis points to two external "pressure points": firstly, the appreciation of the RMB exchange rate to its highest level in nearly three years, which directly impacts the competitiveness of export prices; and secondly, the United States, a core export destination, still has high inventory levels and weak purchasing demand.

The sustained low prices of tilapia for the past six months have severely eroded the profits of fish farmers, leading some to exit the business or significantly reduce the number of fry they stock for the next breeding cycle. This has fueled a strong expectation in the market: that the resulting supply contraction will inevitably trigger a retaliatory price increase.

However, some voices within the industry are warning that this expectation may be overly optimistic. Experienced professionals point out that the underlying structure of the tilapia industry, which is heavily reliant on exports, remains unchanged. A mere reduction in production in certain areas is unlikely to significantly alter the pricing logic dominated by international markets and macroeconomic factors. The tilapia market will not see price increases simply because a few farmers quit or reduce stocking. Production decisions after the Chinese New Year will depend heavily on whether positive changes occur in the "international environment," such as exchange rates and the rate of overseas inventory depletion.

The struggles of domestic aquaculture producers are closely linked to the cautious stance of overseas consumer markets. In the United States, the tilapia wholesale market has recently shown a divergent trend: prices for bigger frozen fillets (such as 5-7 ounces and 7-9 ounces) have slightly decreased due to sufficient inventory held by importers; while prices for smaller size (3-5 ounces) have remained stable due to relatively consistent demand from the food service sector. This divergence indicates that current end-user demand is not entirely weak, but buyers generally lack urgency in replenishing their inventory of larger sizes. This also indirectly confirms the "sufficient inventory in the US" situation, explaining why domestic raw material prices have not yet received upward pressure from demand.

The continuous decline in tilapia prices appears to be a problem of oversupply, but it is actually the result of a combination of "localized disruptions in the global supply chain" and "lagging industrial transformation."

Reference : YUYIPAI

Latest News

-

The price of Golden Pompano is stable high but why the demand and market are going well?After February 24th, 2024, the golden pompano still maintains a good situation of high price operation, and the current stock of fish is limited, and most distributors have almost no inventory in the ...

The price of Golden Pompano is stable high but why the demand and market are going well?After February 24th, 2024, the golden pompano still maintains a good situation of high price operation, and the current stock of fish is limited, and most distributors have almost no inventory in the ... -

New tilapia farming regulations are strictly enforced and prices have soared!In December 2024, prices for farmed tilapia in China have stabilized and are in balance with the US market, a trend that is expected to remain in place until at least January 2025. This stabilization ...

New tilapia farming regulations are strictly enforced and prices have soared!In December 2024, prices for farmed tilapia in China have stabilized and are in balance with the US market, a trend that is expected to remain in place until at least January 2025. This stabilization ... -

The recovery in China's tilapia exports fails to mask the supply pressure.The price trend of the main tilapia producing areas in southern China is differentiated, showing a different pattern : "Price decrease in Guangdong, Price increase in Guangxi, and Price is stabel...

-

Our Delicious Breaded Tilapia Fillet - The Perfect Addition to Your Menu!We hereby recommend Breaded Tilapia Fillet, which is sure to be a hit with your customers and elevate your menu to new heights. Our Breaded Tilapia Fillet is made from the finest quality tilapia fish,...

Our Delicious Breaded Tilapia Fillet - The Perfect Addition to Your Menu!We hereby recommend Breaded Tilapia Fillet, which is sure to be a hit with your customers and elevate your menu to new heights. Our Breaded Tilapia Fillet is made from the finest quality tilapia fish,... -

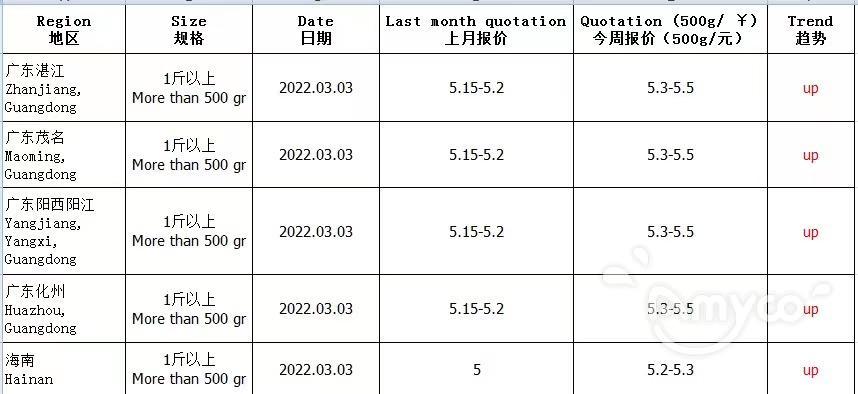

China Tilapia prices are going up after the Chinese New Year holidaysThe following content is my subjective opinion, for reference only: Tilapia Fish prices are going up. When the Chinese New Year just passed, in fact, the general Tilapia fish price was around 5.15 yua...

China Tilapia prices are going up after the Chinese New Year holidaysThe following content is my subjective opinion, for reference only: Tilapia Fish prices are going up. When the Chinese New Year just passed, in fact, the general Tilapia fish price was around 5.15 yua...